As a business owner, you might be shying away from loans because of the stories you’ve heard from others. However, not every loan will be the main reason for bankruptcy. Most likely than not, it’s mismanagement of funds that led to the bankruptcy of certain small businesses.

If you’re planning to start a business, you must know how much money you need for yearly operations. Here’s what you need to know about starting a business and how business loans can help you succeed.

Opening a Business

Starting a business requires you to have startup capital. However, not many Americans have the average annual $184,000 needed to sustain a startup. Although your small business might not have this many yearly expenses, it’s good to make it your potential benchmark. That is if you’re planning to stay in business for the next five years.

For one, $184,000 is a lot of money if you think about it. You’re going to need some help to attain it. Your best option at this point is to either reduce your costs by decreasing the number of employees you have (as payroll takes up a majority of your expenses) or you can get a business loan to grow your business.

Business loans are essential for every growing small business. You might not think about it now, but it’ll eventually pop into your radar once you’ve grown substantial enough. Even small companies that don’t need a business loan get it for their future success. This is called pro-active borrowing, which many innovative entrepreneurs use. Before discussing how to use a business loan efficiently, we first have to discuss the nature of business loans.

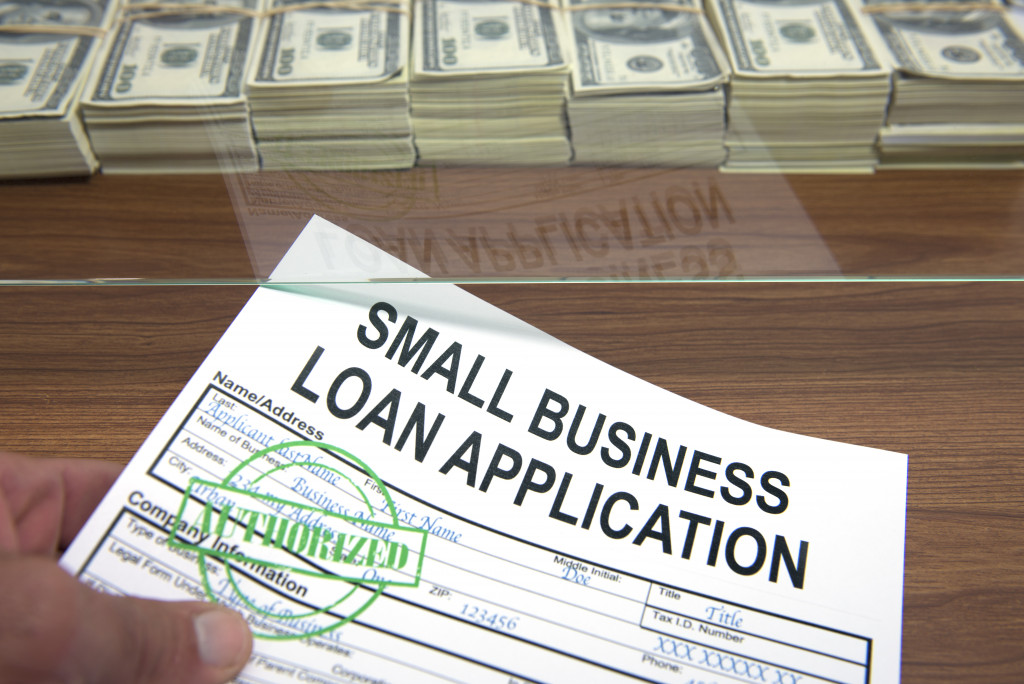

Business Loans

Business loans are self-explanatory. You get a business loan for your company. Some get it to keep their business afloat, while others do it to grow their business. It’s a simple loan and one that, if used correctly, can drive your business to success.

Currently, the interest rate of business loans is lower than ever. The economy is recovering, so there is a need to aggressively decrease interest rates so more people will borrow funds for their business. Moreover, the pandemic has pushed specific organizations to help small businesses. One particular organization giving affordable business loans to people is the Small Business Administration (SBA).

The SBA provided two specific business loans for pandemic relief. The first is the Paycheck Protection Program, which ensures that your employees will get paid. This program has been canceled due to the number of companies that require it, but it might come back soon. The second is the Economic Injury Disaster Loan (EIDL) which gives funds to industries that have suffered the most due to the pandemic. Once again, this program is over, but it might come back again.

Aside from these loans, the SBA offers standard business loans at 3%. It’s one of the lowest interest rates in the market. Still, they also only provide the smallest loans, with the highest reaching only $100,000.

How to Use Them Efficiently

Utilizing business loans can be an intelligent way to grow your business. As stated earlier, some business owners borrow money even if they don’t need it for one prime reason: credit score.

A small company will eventually need to borrow money, and the pandemic has shown that. No business was safe from the pandemic, and those that didn’t have a credit score because they played their hand conservatively suffered for it.

Having a good credit score can mean access to better business loans at a much lower rate. This can save your company from bankruptcy, which is why people borrow business loans even if they don’t need them.

Another way to use business loans efficiently is when you’re planning to expand. Using your business’ money for expansion can be pretty risky. So you want to use borrowed money instead. Business loans still have months before you fully pay them, which means you can test whether the expansion is profitable or not. If not, you can always choose to stop the expansion and pay whatever money you’ve used back to the lender.

What’s Better Than Business Loans?

However, business loans aren’t your only option for expanding your business. One option that savvy entrepreneurs use is their mortgage.

Your paid mortgage can help you start and maintain a business through refinancing. The country is currently experiencing the best mortgage rates, making it the primetime to refinance your mortgage for your business. It’s better than a business loan because you can decrease your interest rate to as low as 1 percent. You can also dictate how much you have to pay monthly to dictate your pacing.

Utilizing loans to grow your business is a smart move and one you should consider doing this year. It’ll make your business grow faster than ever before.